Minimis Safe Harbor Roof Replacement

Application Of Partial Asset Dispositions And The De Minimis Safe Harbor

Irs Tangible Propert Regulations

Tangible Property Regulations An Mps Cpa Presentation

Take Advantage Of New Tax Break For Repairs And Maintenance And Capitalized Assets

Safe Harbor Methods Personal Belongings Markham Norton Mosteller Wright Company Pa

Key Aspects Of The New Tangible Property Regulations

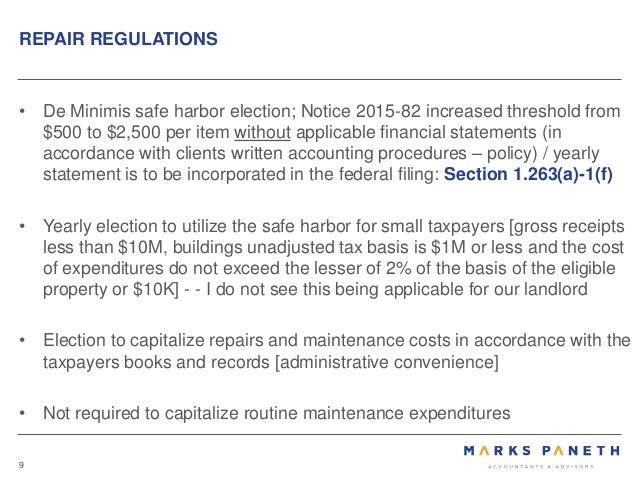

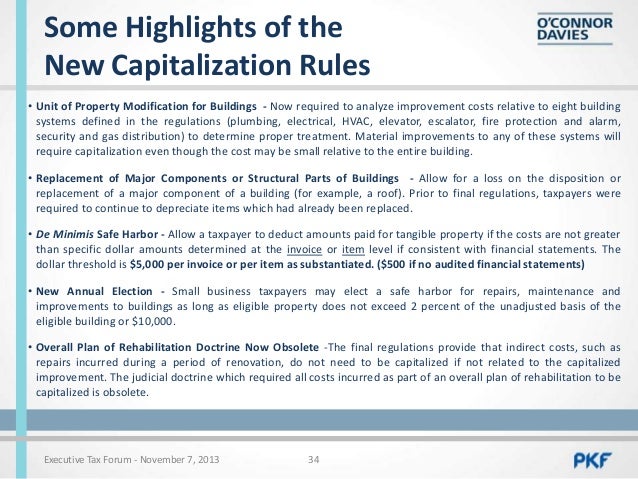

1 2016 but use of the new threshold won t be challenged in tax years prior to 2016 and if a taxpayer s use of the de minimis safe harbor is an issue under consideration in examination appeals or before the u s.

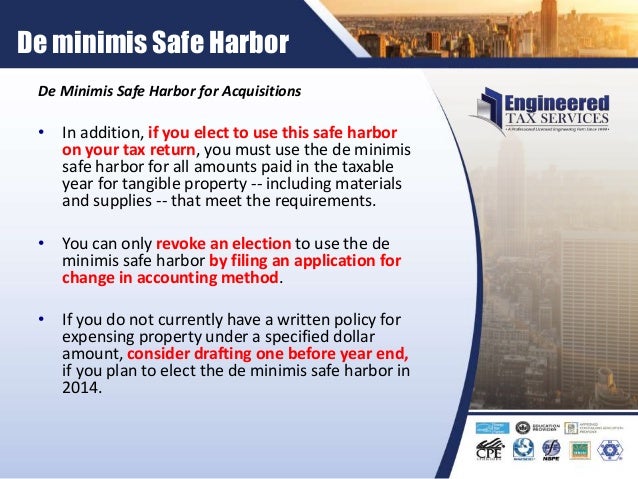

Minimis safe harbor roof replacement. This increase is effective for costs incurred during tax years beginning on or after jan. The de minimis safe harbor election eliminates the burden of determining whether every small dollar expenditure for the acquisition or production of property is properly deductible or capitalizable. A business with an applicable financial statement however has a safe harbor amount of 5 000. De minimis safe harbor election.

A person or business can immediately deduct repair and maintenance expenses if the cost is 2 500 or less per item or per invoice. The de minimis safe harbor can be used to deduct in one year the cost of personal property and building components used in a rental activity. For more information on electing and using the de minimis safe harbor for tangible property see chapter 1 of pub. Safe harbor for routine maintenance.

This expense is a capital improvement which makes the decision and the calculation a bit more complicated. You do have an option of using the safe harbor election if you qualify. However for most landlords this safe harbor is limited to items that cost no more than 2 500 a piece. There is another alternative to the routine maintenance safe harbor.

A taxpayer may elect a de minimis safe harbor to deduct the amounts paid to acquire or produce tangible property up to a dollar threshold. 1 a safe harbor for small invoices. Using the deduction under the de minimis safe harbor election is definitely the best option. Tax court in a tax year beginning after dec.

If you elect to use the de minimis safe harbor you don t have to capitalize the cost of qualifying de minimis acquisitions or improvements. The amounts allowable under the de minimis safe harbor are 2 500 or 5 000 depending on whether the taxpayer has an applicable financial statement afs. If you determine that your cost was for an improvement to a building or equipment you still may be able to deduct your cost under the routine maintenance safe harbor. All expenses you deduct using the de minimis safe harbor must be counted toward the annual limit for using the safe harbor for small taxpayers the lesser of 2 of the rental s cost or 10 000.

But in spite of this understandable frustration and confusion the new regulations provide one noteworthy loophole that both tax accountants and taxpayers need and will want to understand. The new tangible property regulations in effect for 2014 and later years mostly frustrate tax accountants and mostly confuse small businesses and real estate investors. This is up from 500 which was the threshold through december 31 2015.

Are You Ready For The New Tangible Property Rules

Https Www Bdo Com Getattachment Cce22f03 0eb9 4dda 824e Fb8f9bdad1e8 Attachment Aspx

Https Www Claconnect Com Workarea Downloadasset Aspx Id 8716

N Overview Of Tangible Property Regulations N Greatest Impacts To Your Clients N Avoid The Traps Of The Temporary Regs N Action Steps To Prepare For Ppt Download

Optimizing Residential Real Estate Deductions Journal Of Accountancy

1 Equipment And Supplies Presently Being Expensed Under A Minimum Capitalization Policy Pdf Free Download

Https Www Cohencpa Com Cohensite Media Cohenredesign Image Gallery Events Documents Managing Capitalization Webinar Pdf

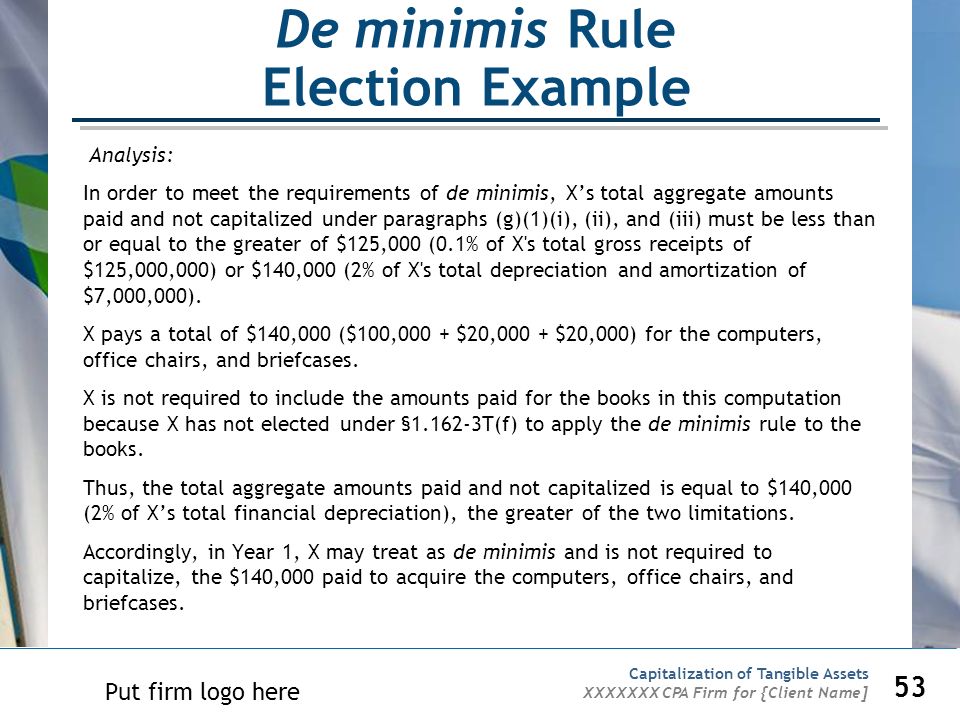

Capitalization Of Tangible Assets Xxxxxxxxxx Cpa And Xxxxxxx Cpa Ppt Download

Irs Increases Small Asset Expensing Safe Harbor Articles Resources Cla Cliftonlarsonallen

Put Firm Logo Or Letter Head Here Capitalization Of Tangible Assets Understanding The New Irs Regulations And What Client Name Needs To Do In Response Ppt Download

Final Tangible Property Dauby O Connor Zaleski Llc Doz Has Been In Business For 27 Years Has 150 Employees And Specializes In Ppt Download

2014 Tax Savings Delivered Cost Segregation Tpr Implementation The Implementation Of The Tangible Property Regulations Cost Segregation Services Ppt Download

Engineered Tax Services Lunch Workshop

Depreciation Refresher 2017

Http Www Klcpas Com Wp Content Uploads 2014 11 Mcgowan Tpr Presentation Outline Pdf

Https Costsegexperts Com Wp Content Uploads 2019 10 Webinar Repair Regulation Fall 2019 Pdf

Https Assets Kpmg Com Content Dam Kpmg Pdf 2015 08 Tax Notes Repairs March 2012 Pdf

Understanding The Safe Harbor Rules And Keeping Money In Your Pocket

Routine Maintenance Safe Harbor

Complying With The Tangible Property Regulations Mission Impossible

Tax Guide Cpa For Real Estate Investors Real Estate Tax Accountant

Here Are Tax Tips For Hurricane Victims Khou Com

Ex 1 2 Ex1 Htm Exhibit 1 Exhibit

Farm Taxes Deducting Expenses An Overview Agfax

What We Know About New Tax Changes For 2017 So Far Tom Copeland S Taking Care Of Business

Irs Expands Write Offs For Self Storage Owners Learn About New Safe Harbors Inside Self Storage

Why Our Tax Code Loves Real Estate Investors Prei 284 Passive Real Estate Investing

What Taxpayers Need To Know To Comply With The Final Tangible Property Regulations

Nonprofit Organizations And The Tangible Property Regulations Bkc Cpas Pc

What The New Tangible Property Regulations Mean To You Dermody Burke Brown

Irs Tangible Property Rules May Help Construction And Real Estate Industry Articles Resources Cla Cliftonlarsonallen

Https Www Gpo Gov Fdsys Pkg Cfr 2012 Title26 Vol3 Pdf Cfr 2012 Title26 Vol3 Sec1 263a 3t Pdf

Understanding The Irs S New Math For Landlord Repairs Inman

Year End Tax Planning Strategies For Businesses Lvbw

Https Www Currentfederaltaxdevelopments Com S Depreciation And Fixed Assets Slides 6w9w Pdf

Cpfa73uk02qpfm

Tangible Property Repair Regulations Tax Insights Kbkg

Https Www2 Deloitte Com Content Dam Deloitte Us Documents Tax Us Tax Client Summary Deconstructing The Tangible Property Regs 101813 Pdf

Capitalizing On Equipment Repairs

Three Safe Harbors All Landlords And Real Estate Investors Should Know About

Http Taxworkbook Com Files 2015 09 Agriculture Pdf

Repairs Maintenance Traderstatus Com

Corporate Tax Update